Not too long ago, the FinTech industry in the Middle East was on the brink of expansion as digital technologies became more rampant and cashless payments rose in popularity.

It is now a flourishing industry today enabled by digital transformation services that are giving FinTech companies the technology support they need.

The Middle East region is now the focus of top FinTech software development companies as startups continue to emerge.

It is all set to attract $2 billion worth of investment in the next few years with almost half of its population young and tech-savvy.

From just 1 percent of global FinTech investment, the FinTech sector is now growing at a CAGR of 30 percent that is likely to accelerate further.

A rapidly developing eCommerce sector that is now growing at an annual rate of 33 percent gives further impetus to the FinTech growth in the Middle East.

Clearly, the FinTech scene is magnetic in the Middle East and is drawing both investments and attention.

The stage is set for growth and innovation

The UAE and Bahrain hold leading positions now when it comes to venture capital investments having attracted almost $90 million in FinTech funding in the period between 2010 and 2017.

Those like PayTabs and Bayzat have already established themselves in the region facilitating payments, remittances, lending, and banking.

Bahrain FinTech Bay is reputedly the first and the largest FinTech hub in the Middle East and Africa while many others are spreading roots gaining a firm foothold in the region.

With ALGO Bahrain already planning to launch 15 FinTech platforms by 2022, Bahrain surely has become a sought-after destination for FinTechs.

Dubai too boasts of the Dubai International Financial Centre (DIFC) that is scaling up innovation and growth in the FinTech sector.

Fueled by government-driven funding programs like the US$100 million DIFC Fintech Fund, it is paving the path for a thriving FinTech ecosystem.

Saudi is also making significant contribution with the Saudi Arabian Monetary Association (SAMA) launching Fintech Saudi that has enabled 21 FinTech companies to join the Sandbox.

Meanwhile, Irish FinTech leader Global Shares has expanded its presence with a new office in Riyadh, Saudi Arabia offering web-based software solutions and other Irish firms are keen on claiming their share of the market in the Middle East region.

Explains Abdulhadi Alherz, managing director of the Middle East for Global Shares, “Saudi Arabia has a large, strong economy with a population of 33.7 Million and a GDP of $790tn.

Our country is highly diverse: 32% of the population is made up of expats and 66% of the population is youthful, both of which will help from a long-term incentive plans perspective.”

Besides, the government too is offering immense support through concerted efforts and initiatives in the form of funding, research programs, and accelerator schemes to support FinTech and make it a thriving ecosystem.

KSA, Bahrain, Qatar, and UAE are rolling out FinTech strategy programs to encourage the adoption of digital solutions and banking industry solutions and have as many FinTech service providers too to further this cause.

The fact that residents are eager to explore FinTech solutions is a big boost to the FinTech industry.

Mobile wallets and online payments are now preferred and a high mobile penetration rate has opened new opportunities for it to explore.

Payment preferences go from cash to digital

1 in 9 transactions in the Middle East and Africa (MEA) region at the point of sale (POS) is now contactless and Mastercard has recorded an increase of over 66 percent in contactless payments in MEA.

Globally, contactless payments are expected to grow to $18 billion by 2025 putting the spotlight on the growing popularity of this mode of payment.

The payments landscape is evolving and it is safe to assume that the shift to digital is going to be permanent.

The growth in tech and telecom and their reach and technological prowess are facilitating digital payments in a big way.

As per a Mckinsey survey, 90 percent of respondents believed at least half of the new users will prefer to stick to digital payments, and more than 50 percent increase in digital transactions is expected in the next five years as compared to the numbers garnered in 2020.

The flight from cash to digital has undoubtedly popularized digital wallets and FinTech solutions like never before.

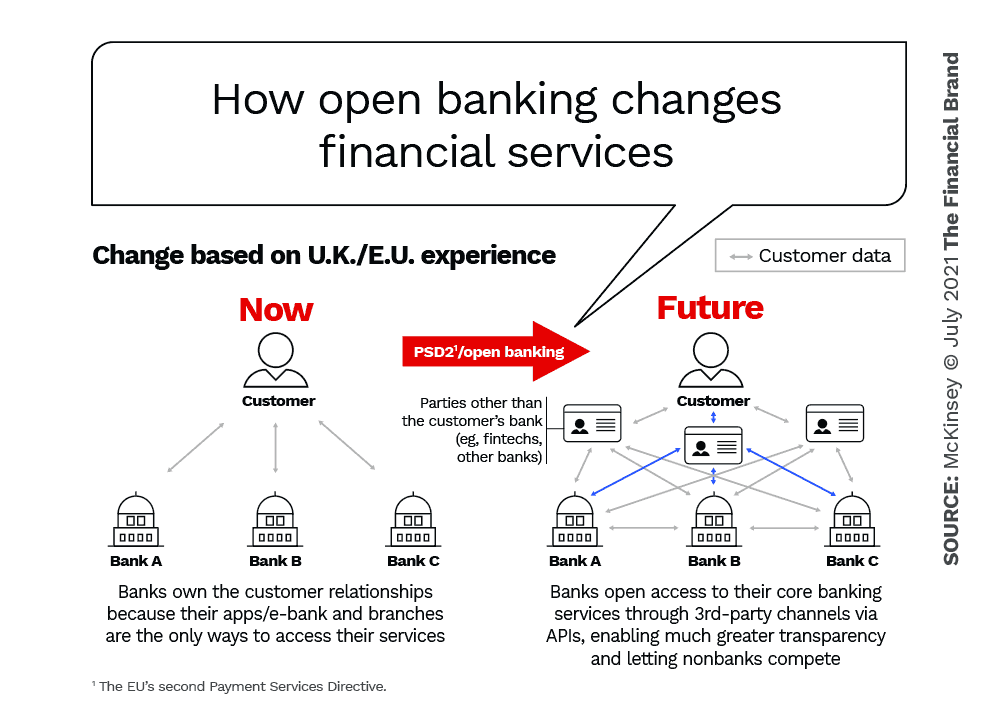

Open banking gains momentum

Open banking has been received with open arms by customers, banks, government agencies, and third parties in several countries though the Middle East was a slow adopter.

Things started changing considerably after Bahrain commenced its Open Banking journey in 2018 and introduced a Bahrain Open Banking framework in 2020.

Saudi Arabia is expected to follow suit in 2022.

What’s more; a lot is still being done on the design and implementation front to build a solid open banking ecosystem.

The pandemic has significantly contributed towards its growth while digitally-savvy residents are eager to explore its benefits.

Open banking solutions typically rely on application programming interfaces (APIs) that enable seamless transactions for users.

Tarabut Gateway, for instance, connects banks and FinTechs through a single, universal Open Banking API that facilitates transactions and payments through a global network.

Open Banking allows financial services to access KYC information in one place thereby eliminating laborious verifications while onboarding new customers. Customers, on the other hand, are able to view all their financial information pertaining to savings accounts, credit cards, loans, and investments.

The use of APIs to leverage real-time or near-real-time data is also helping financial services mitigate risks.

Banks embrace digital transformation

Banks have dominated the financial sector for the longest time but modern customers are now willing to give nonbank players a chance too.

A region that has relied on in-person communication and service is now willing to consider digital business models of banking.

The pandemic has accelerated this acceptance and banks are now willing to partner with FinTech software development companies to accelerate their digital journey.

This does not mean that banks are no longer needed but the fact is that there are now more avenues for everyone to thrive.

Banks merely need to change their perspective and adjust their focus.

They need to view FinTechs as partners and collaborators rather than competitors.

As Anthony Yazitzis, a financial services and Fintech partner at Deloitte explains, ”In the Middle East banking sector, FinTechs are considered as legitimate players of an emerging ecosystem.

However, to date, they have yet to be deployed by banks as their strategic partners.”

Banks need to digitize customer journeys and use technologies like advanced AI and advanced analytics to get the necessary information to offer value-added services.

As regulatory changes allow entry to new players, it is imperative for banks to invest in activities that build trust in their services and solutions.

They need to address pain points across use cases to offer the required support digitally.

Banks need to invest in digital transformation to usher in a fresh perspective on onboarding new customers and reinventing at different stages to serve them better.

Traditional banks have been less focused on technology and innovation but the Fintech revolution is now forcing them to change this mindset and adapt to innovate and grow.

Collaboration is the key

Modern customers expect greater customization and better services that can be easily achieved by integrating banking with FinTech.

While both differ in their unique selling propositions, they can collaborate for a better reach and experience.

FinTech can bring along disruptive ideas and technologies while banks will come with their ability to drive customer demand and a loyal customer base.

Banks should identify the service gaps and areas that have growth potential and accordingly find a suitable FinTech partner to build capabilities.

This can be a win-win for both as banks transcend from consumer banking to digital banking.

The current financial environment is suitable for collaboration as both banks and financial institutions prepare themselves to attain ambitious digitization goals.

While trust building will continue to remain an important endeavor, developing the right value proposition and customer experience will be of paramount importance to promote banking industry solutions.

The collaboration and the merging of strengths and competencies will lead to:

- Safer transactions

- New ventures

- Broad portfolio

- Equipped for change

1. Safer transactions

Banks possess the necessary customer information but in partnership with FinTechs, they can leverage their technology to ensure the security of transactions while continuing to remain the transaction authenticating authority.

2. New ventures

With joint investment and capabilities, the partnership can help them come up with accelerator programs to improve different aspects of banking.

3. Broad portfolio

A wide range of offerings can be made available to customers to survive the competition and enable greater comfort, speed, and cost benefit for every transaction.

4. Equipped for change

With pooled synergies, banks and FinTechs will be better prepared to manage the changing consumers' expectations and market fluctuations.

Summing up

The FinTech industry is booming despite a rather slow global economy.

There is plenty of room for new players though the competition is stiff thanks to an ever-expanding tech stack.

FinTech companies are now preferred by younger demographics that value ease and convenience.

With speedier transactions and a superior customer experience, FinTech solutions have become an important aspect of personal finance management.

FinTech startups as well as giants have partnered with the best digital transformation company to obtain technology support and grow their business.

The top digital transformation services can help develop strategies, create value, and address the unique requirements of diverse target segments in the world of finance effectively.

Share this

What is The Impact of Web3.0 on the Fintech Industry

How FinTech drives Innovation and Transformation in Financial Services